Interest Rates Are Dropping—Is Now the Right Time to Buy or Refinance in Michigan?

Erik Gascho • August 7, 2025

This is a subtitle for your new post

After months (or let’s be honest—years) of higher mortgage rates, there’s finally some good news for those waiting on the sidelines: Interest rates are starting to come down, and the Federal Reserve is widely expected to cut rates in September.

Whether you're a first-time homebuyer in Clarkston, looking to refinance your existing mortgage in Michigan, or just trying to make sense of what’s going on with rates, this update is for you.

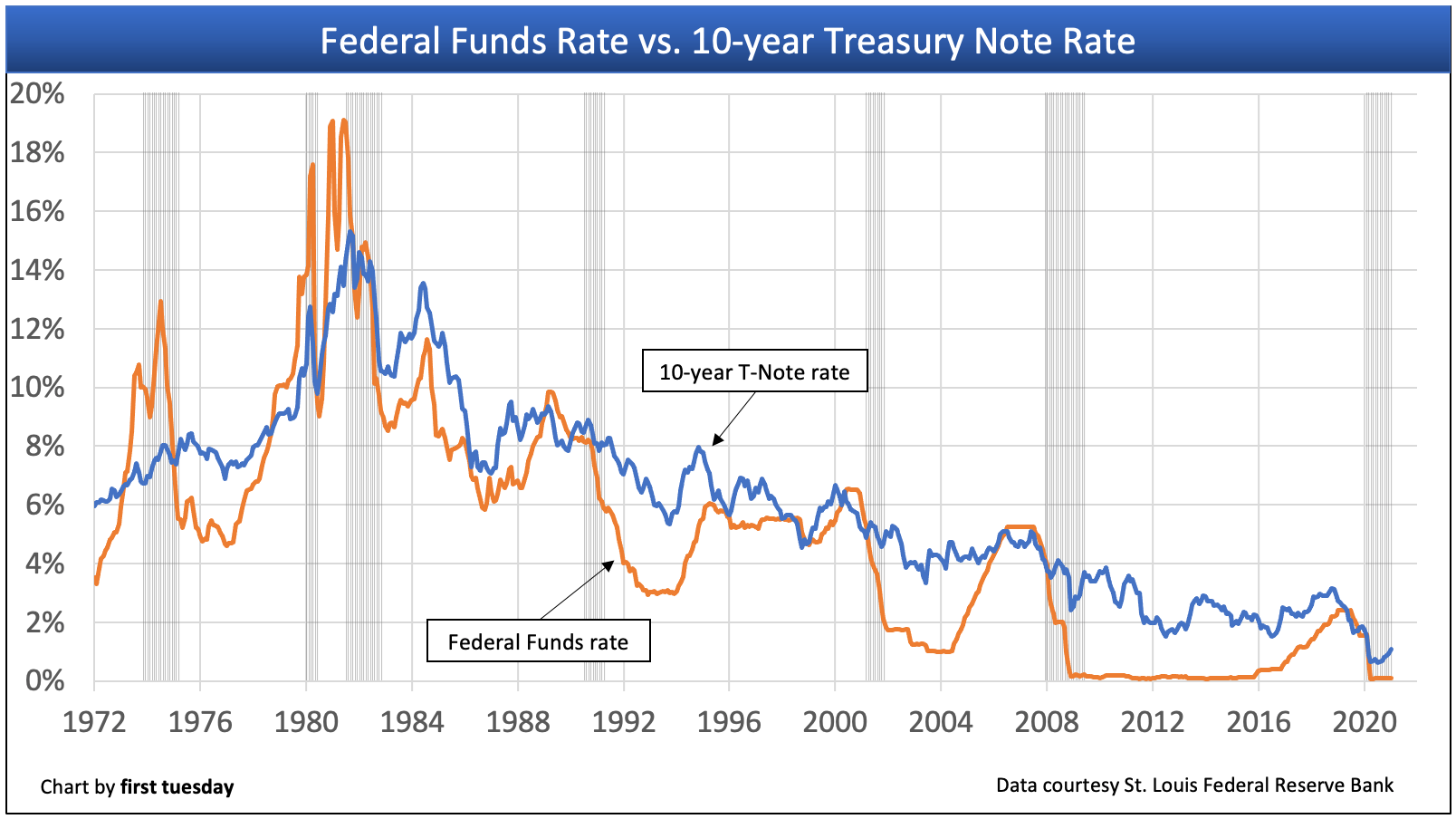

📉 What’s Happening With Interest Rates Right Now?

Over the last few months, inflation has shown signs of cooling, and the job market is gradually softening—exactly the combination the Federal Reserve wants to see before lowering rates.

As a result:

Mortgage rates have been trending downward, with 30-year fixed rates dropping closer to the mid-6% range.

Many experts (and futures markets) predict the Fed will make its first rate cut in September 2025, with potentially more to follow if inflation continues to behave.

For context, just a year ago, many buyers in Southeast Michigan were looking at 7%+ interest rates. So, even a drop of half a percent or more can make a major difference in monthly payments and long-term savings.

🏡 What This Means for Michigan Homebuyers

If you’ve been holding off on buying a home in Clarkston, Lake Orion, or Rochester Hills because of rates—this might be your window.

Here’s why:

Lower monthly payments: A 0.5% drop in interest rate on a $300,000 mortgage could save you roughly $100–$150/month.

More purchasing power: Lower rates increase how much home you can afford without stretching your budget.

Less competition (for now): Many buyers are still waiting. Getting pre-approved before the rush can help you secure a better deal.

💡 Pro Tip: Consider getting rate-locked before rates fall further—some lenders offer a float-down option if rates drop again before closing.

🔄 What About Homeowners Looking to Refinance?

If you purchased or refinanced during the 2022–2024 rate spikes, you may now have an opportunity to restructure your mortgage for better cash flow.

Refinancing might make sense if:

Your current rate is over 7%

You want to consolidate high-interest debt

You’re looking to access home equity for renovations, tuition, or investing

You’re planning to stay in your home for at least 3 more years

Even if you're unsure if now is the right time, it’s worth exploring what a refi could look like based on your long-term goals and financial plan.

📊 Should I Wait for Rates to Drop Even More?

That’s the big question everyone’s asking. Here’s my honest take:

Yes, rates may continue to fall in 2025 if inflation stays low.

But, as rates drop, more buyers will flood the market, driving up home prices and competition.

Timing the market perfectly is nearly impossible. Instead of waiting for “perfect” conditions, think about your personal situation:

Do you have stable income and job security?

Are you tired of renting or outgrowing your current home?

Would locking in today’s rate give you more peace of mind?

If the answer is yes, this market could offer a smart opportunity—especially with expert guidance and a custom plan.

🤝 Local Expertise You Can Trust

As a Clarkston-based mortgage advisor and lifelong Michigander, I work with families and financial professionals across Oakland County and beyond. Whether you're in Clarkston, Oxford, Waterford, or Bloomfield Hills, I can help you:

Understand your numbers

Get pre-approved with confidence

Lock in a rate strategy that protects you long-term

Decide whether buying, refinancing, or waiting makes the most sense for you

✅ Ready to Explore Your Options?

📅 Schedule a free mortgage strategy session with me:

👉 erikgascho.youcanbook.me

You’ll walk away with clarity, a plan, and zero pressure.

Let’s make the most of this rate shift—together.

For decades, most mortgage lending has relied on Classic FICO.

Classic FICO gives lenders a snapshot of your credit at one point in time. It looks at things like payment history, balances, length of credit, credit mix, and recent credit activity.

Many homeowners feel stuck.

On one hand, you may have a mortgage rate that’s far lower than today’s market rates. Giving that up can feel like a mistake.

Homeownership is not just about getting the keys.

It is about caring for the place you live, protecting the investment you made, and making smart financial decisions along the way. At NEO Home Loans, we believe successful homeownership is built one month at a time through education, planning, and proactive support.

Do we make an offer and hope everything works out?

Do we wait and risk losing the home?

Do we rush our current home onto the market?

Unfortunately, this is where many homeowners find themselves.

Nobody wants to feel like they bought at the “wrong time.” Especially after watching headlines bounce between “housing crash,” “record prices,” and “rates are too high.”

If you’re thinking about moving, you’ve probably run into this problem:

You want to buy your next home…

But you feel like you have to sell your current one first.

When most people look at a mortgage payment, they only see what it costs today.

But that may not be the best question.

A better question could be:

What will this same payment feel like 10 years from now?

The housing market is changing… and most buyers haven’t caught up yet.

For the past few years, sellers had all the control. Homes sold fast. Buyers competed aggressively. And negotiating power was almost nonexistent.

That’s no longer the case.

Today, we’re seeing a clear shift toward a more balanced market, and that creates opportunity if you know how to use it.

If you’re planning to buy a home this season, you’re stepping into a market full of opportunity.

More homes are coming to market. Activity is picking up. And it finally feels like you might have a real shot at finding the right home.

But there’s a challenge most buyers don’t realize until it’s too late.

Discover why focusing only on interest rates can cost Michigan homeowners thousands. Learn how mortgage strategy impacts long-term wealth.