“Marry the House, Date the Rate”: What This Mortgage Mantra Really Means (And Why It Matters in Michigan)

Erik Gascho • July 24, 2025

What Does “Marry the House, Date the Rate” Mean?

If you’ve been house hunting or talking to real estate professionals in Clarkston or anywhere in Metro Detroit, you’ve probably heard the phrase “Marry the house, date the rate.” But what does it actually mean—and is it good advice?

Let’s break it down in simple terms:

“Marry the House” means you should buy the home you truly love—the one that fits your needs, lifestyle, and long-term goals. This is a long-term commitment.

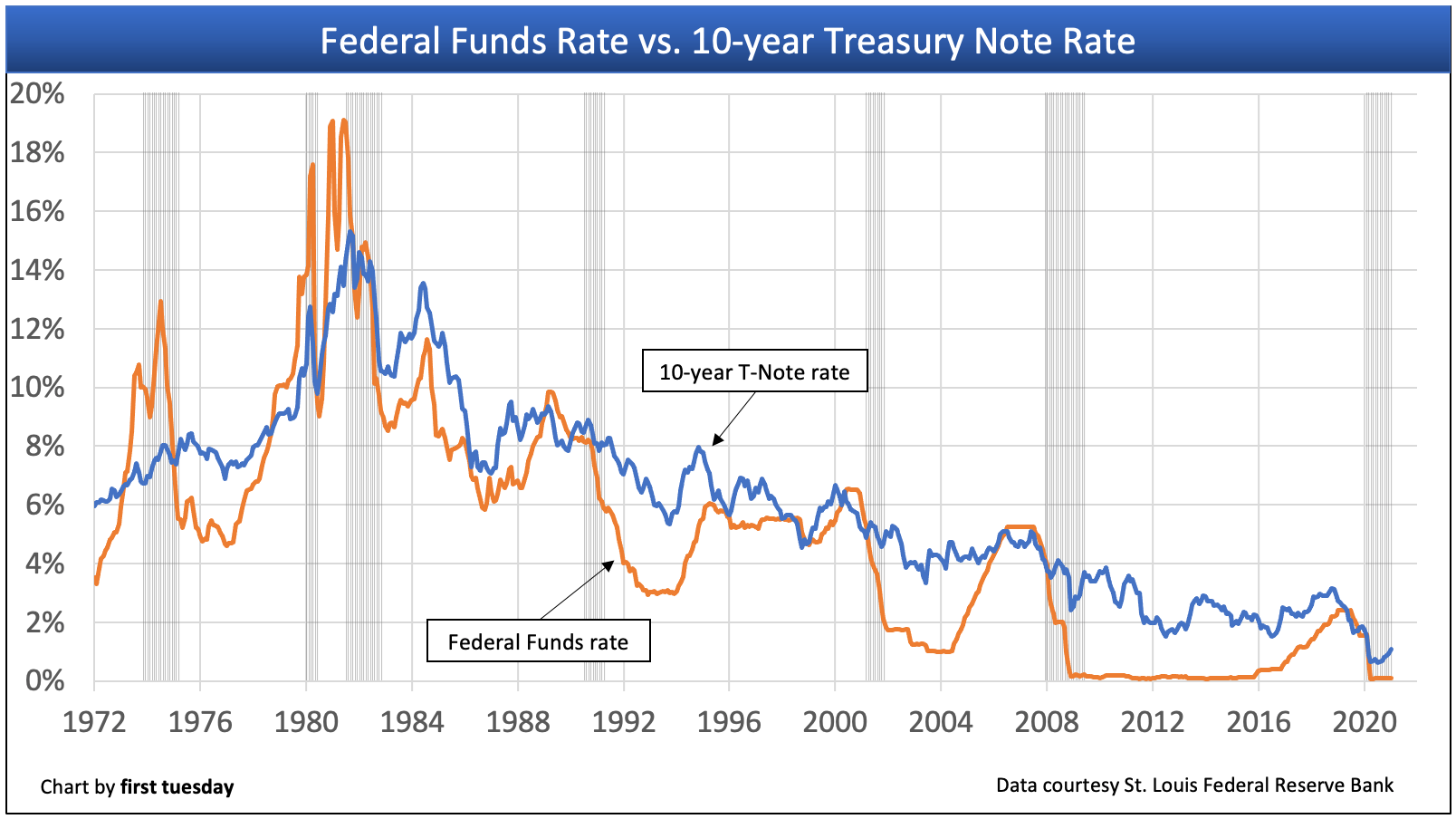

“Date the Rate” means your mortgage interest rate is temporary—you’re not stuck with it forever. When rates go down, you can refinance.

In other words, don’t miss out on your dream home just because rates are higher right now. You can always refinance later. But that house? It might not be available later.

Why This Mindset Matters in Today’s Market

Interest rates have been fluctuating over the past year, and if you’re like many buyers in Clarkston, Waterford, or Lake Orion, you’re asking:

“Should I wait for rates to drop before buying?”

Here’s why that could be a risky strategy:

Home prices in Michigan are still rising. In areas like Clarkston and surrounding suburbs, we’re seeing steady appreciation. Waiting could mean paying more later.

You can’t refinance a home you don’t own. Lock in the house now and refinance when the market shifts.

Inventory is tight. The right home in the right school district doesn’t stay on the market long.

🏠 Let’s say you buy now at 7.0% interest and refinance to 5.5% a year from now. That’s a win—especially if your home has gained value in the meantime.

Real Example: Clarkston Buyer Case Study

A recent client of mine here in Clarkston found a home they loved in early spring. Rates were around 6.875%, and they were hesitant.

We talked through their long-term goals, crunched the numbers, and made a plan to refinance when rates drop. They’re now in their dream home—and building equity every month. If they had waited, that same home would’ve cost $15,000 more based on local appreciation trends.

What to Ask Yourself Instead of “Should I Wait?”

Can I afford the payment today, and does it fit my monthly budget?

Is this a home I can grow into over the next 5–10 years?

If I wait, will I still be able to afford the same neighborhood?

Remember, a mortgage isn’t a lifelong sentence. But missing out on the right home can set your goals back years.

What’s the Plan? Here’s How I Help:

At NEO Home Loans powered by Better, I help Clarkston families build smart, flexible mortgage strategies. When you work with me, you get:

✅ A plan for refinancing when rates drop

✅ An analysis of total cost of waiting vs. buying now

✅ Guidance through a competitive local market

✅ Local experience with homes in Clarkston, Lake Orion, Waterford, and surrounding areas

Let’s run the numbers together and see what’s possible.

Want to Talk It Through?

Schedule a free planning call with me today. I’ll walk you through options tailored to your goals—no pressure, just clear advice.

📅 Book a time on my calendar

📞 Or call/text me at 248-214-8526

Final Thought

Rates will change. Homes will come and go. But the right house at the right time? That’s worth acting on.

Marry the house. Date the rate. And let’s build your mortgage plan together.

For decades, most mortgage lending has relied on Classic FICO.

Classic FICO gives lenders a snapshot of your credit at one point in time. It looks at things like payment history, balances, length of credit, credit mix, and recent credit activity.

Many homeowners feel stuck.

On one hand, you may have a mortgage rate that’s far lower than today’s market rates. Giving that up can feel like a mistake.

Homeownership is not just about getting the keys.

It is about caring for the place you live, protecting the investment you made, and making smart financial decisions along the way. At NEO Home Loans, we believe successful homeownership is built one month at a time through education, planning, and proactive support.

Do we make an offer and hope everything works out?

Do we wait and risk losing the home?

Do we rush our current home onto the market?

Unfortunately, this is where many homeowners find themselves.

Nobody wants to feel like they bought at the “wrong time.” Especially after watching headlines bounce between “housing crash,” “record prices,” and “rates are too high.”

If you’re thinking about moving, you’ve probably run into this problem:

You want to buy your next home…

But you feel like you have to sell your current one first.

When most people look at a mortgage payment, they only see what it costs today.

But that may not be the best question.

A better question could be:

What will this same payment feel like 10 years from now?

The housing market is changing… and most buyers haven’t caught up yet.

For the past few years, sellers had all the control. Homes sold fast. Buyers competed aggressively. And negotiating power was almost nonexistent.

That’s no longer the case.

Today, we’re seeing a clear shift toward a more balanced market, and that creates opportunity if you know how to use it.

If you’re planning to buy a home this season, you’re stepping into a market full of opportunity.

More homes are coming to market. Activity is picking up. And it finally feels like you might have a real shot at finding the right home.

But there’s a challenge most buyers don’t realize until it’s too late.

Discover why focusing only on interest rates can cost Michigan homeowners thousands. Learn how mortgage strategy impacts long-term wealth.