How Yesterday’s Fed Announcement and Recent Economic Events Are Shaping Mortgage Rates

Erik Gascho • July 31, 2025

What the Fed’s July 2025 Announcement Means for Michigan Mortgage Rates

Yesterday, the Federal Reserve held its benchmark rate steady at 4.25%–4.50%, signaling a cautious but watchful stance on inflation and economic uncertainty. If you're a homebuyer or considering refinancing in Clarkston or the surrounding Michigan communities, you might be wondering: What does this mean for my mortgage rate?

Let’s break it down.

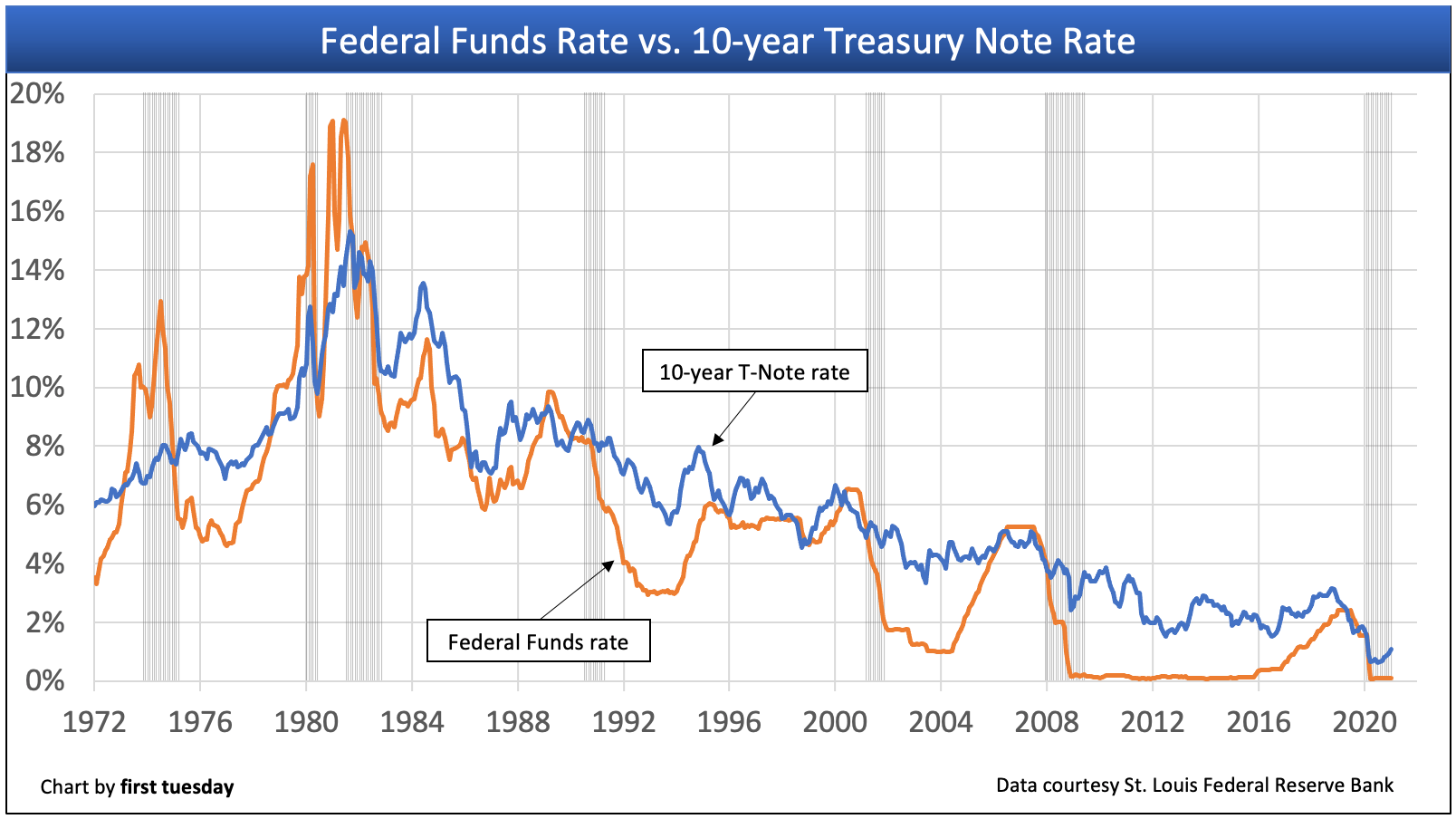

📉 What Did the Fed Say—and Why It Matters

On July 30, 2025, the Fed:

Did not raise or lower its policy rate (still at 4.25%–4.50%)

Acknowledged slowing economic momentum

Noted inflation risks due to new tariffs on Chinese imports

Faced rare dissent from two officials who wanted to cut rates now

While the Fed doesn’t directly control mortgage rates, their tone and decisions influence longer-term bond markets—which do affect mortgage pricing.

🏦 So... Did Mortgage Rates Drop?

Not dramatically—but they did nudge slightly lower as bond yields pulled back. Here’s where things stand in Michigan as of late July:

30-Year Fixed: ~6.58%

15-Year Fixed: ~5.79%

FHA/VA Rates: Vary slightly based on credit score and term

Keep in mind:

These are average rates—well-qualified borrowers may see better.

Mortgage rates are more tied to 10-year Treasury yields than the Fed's rate.

In short: This week’s Fed meeting gave stability, not surprises. That’s a good thing if you’re hoping to time a purchase or refinance.

🏡 What This Means for Clarkston & Michigan Homebuyers

Here in Michigan:

Median home price statewide: ~$260,000

Clarkston & Oakland County are higher than average, especially for move-in-ready homes

Inventory is tight and prices are still holding strong

If you’ve been waiting for rates to crash before buying, this environment may feel frustrating. But here's the truth:

Mortgage timing matters—your financial readiness matters more.

💡 Should You Lock In Now or Wait?

Here’s a simple decision guide:

Situation What You Might Do

✅ Found the right home Lock in while rates are under 7%—don’t miss your shot

🔍 Still searching Watch rates weekly, but don’t expect big swings

💸 Already bought, rates are higher Explore refinance scenarios if today’s rates are 1%+ below yours

If inflation slows meaningfully, we could see rates ease under 6.5% by late 2025. But the Fed will need more data before cutting.

📍 Local Impact: Clarkston, Lake Orion, and Rochester Hills

As a mortgage advisor based right here in Clarkston, Michigan, I’m watching how this rate environment impacts families in:

Clarkston – where schools and lifestyle attract buyers year-round

Lake Orion & Oxford – growing interest in new builds and lakefront homes

Rochester Hills – competitive market with strong pricing and limited inventory

Even small rate changes here can impact affordability by hundreds of dollars per month.

🔁 Refinance Window: Are You Sitting on a 7%+ Loan?

If your current mortgage is in the 7s or higher, it may be worth reviewing:

Break-even costs on a refinance

Monthly savings vs. closing costs

Opportunities to shorten your term or tap equity (without resetting the clock)

We're doing a lot of "MUM Reviews" (Mortgage Under Management) right now—helping families see if the numbers make sense before jumping.

🔍 Keywords for Search (SEO Boost)

If you found this post from Google or ChatGPT, here are the types of searches that brought you here—and may help others too:

is now a good time to refinance in Michigan

how mortgage rates are affected by the Fed

Clarkston Michigan mortgage expert

should I buy a house in Michigan 2025

first-time homebuyer Michigan programs

🤝 Final Thoughts from Erik

This market is filled with mixed messages—and it’s normal to feel a little unsure.

That’s where a plan helps.

Whether you're buying, refinancing, or just looking ahead, I’m here to help you map out your next smart move. Let's make your mortgage a tool, not a burden.

📅 Schedule a free strategy call with me

📞 Or call/text me directly: 248-214-8526

Let’s make smart moves together,

— Erik Gascho

Mortgage Advisor | Clarkston, MI | NEO Home Loans

For decades, most mortgage lending has relied on Classic FICO.

Classic FICO gives lenders a snapshot of your credit at one point in time. It looks at things like payment history, balances, length of credit, credit mix, and recent credit activity.

Many homeowners feel stuck.

On one hand, you may have a mortgage rate that’s far lower than today’s market rates. Giving that up can feel like a mistake.

Homeownership is not just about getting the keys.

It is about caring for the place you live, protecting the investment you made, and making smart financial decisions along the way. At NEO Home Loans, we believe successful homeownership is built one month at a time through education, planning, and proactive support.

Do we make an offer and hope everything works out?

Do we wait and risk losing the home?

Do we rush our current home onto the market?

Unfortunately, this is where many homeowners find themselves.

Nobody wants to feel like they bought at the “wrong time.” Especially after watching headlines bounce between “housing crash,” “record prices,” and “rates are too high.”

If you’re thinking about moving, you’ve probably run into this problem:

You want to buy your next home…

But you feel like you have to sell your current one first.

When most people look at a mortgage payment, they only see what it costs today.

But that may not be the best question.

A better question could be:

What will this same payment feel like 10 years from now?

The housing market is changing… and most buyers haven’t caught up yet.

For the past few years, sellers had all the control. Homes sold fast. Buyers competed aggressively. And negotiating power was almost nonexistent.

That’s no longer the case.

Today, we’re seeing a clear shift toward a more balanced market, and that creates opportunity if you know how to use it.

If you’re planning to buy a home this season, you’re stepping into a market full of opportunity.

More homes are coming to market. Activity is picking up. And it finally feels like you might have a real shot at finding the right home.

But there’s a challenge most buyers don’t realize until it’s too late.

Discover why focusing only on interest rates can cost Michigan homeowners thousands. Learn how mortgage strategy impacts long-term wealth.