How Millennials Can Still Afford a Home in Michigan—Even With High Prices and Rates

Erik Gascho • July 30, 2025

This is a subtitle for your new post

If you’re a Millennial living in Clarkston, Waterford, or anywhere across Metro Detroit, you’re not imagining it—buying your first home today is harder than ever. High home prices, rising interest rates, and stagnant wages have created real challenges for younger buyers trying to break into the market.

But here’s the good news: affordability doesn’t mean impossibility.

As a local Mortgage Advisor based here in Clarkston, Michigan, I work with Millennial buyers every day. Whether you’re feeling stuck renting or unsure if now is the right time to buy, this guide is for you.

💡 Why Is Buying a Home So Hard Right Now?

Let’s break down the pain points:

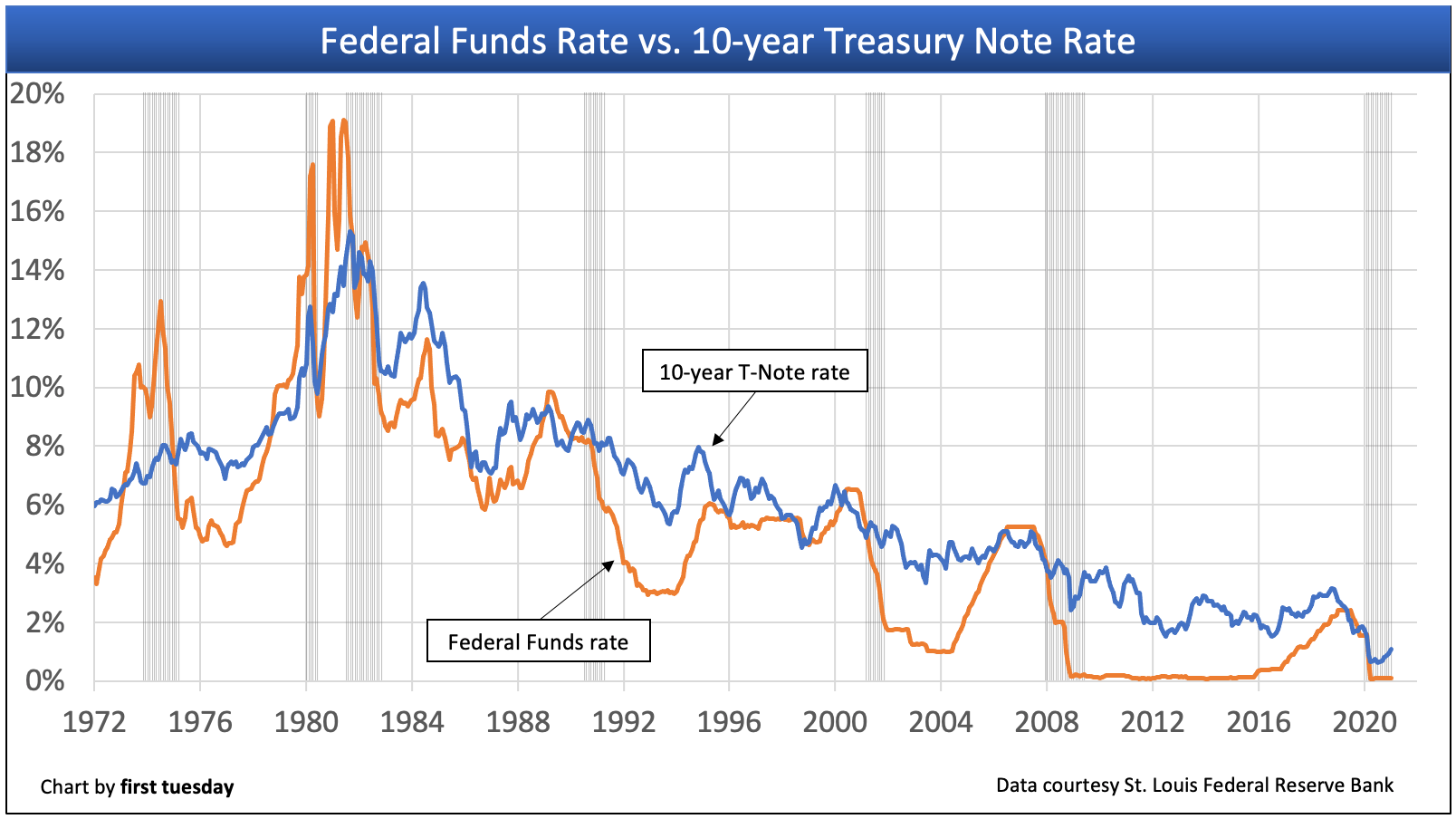

Rising interest rates have made monthly payments jump

Home values across Michigan have increased by over 35% since 2020 (Zillow, July 2025)

Rent is rising too—which means saving for a down payment is tougher than ever

Student loans and other debts are limiting how much buyers qualify for

Sound familiar?

🛠️ 5 Real Strategies Millennials Are Using to Afford Homes in Michigan

Here’s what’s working right now for buyers just like you in Clarkston and nearby communities:

1. Rethink the Down Payment

You don’t need 20% down to buy a home.

In fact, many of our Millennial clients qualify for:

3% down conventional loans

0% down USDA loans (available in many rural parts of Oakland County)

FHA loans with 3.5% down and flexible credit guidelines

👉 We even offer low-down-payment options combined with down payment assistance programs available across Michigan.

2. Get Pre-Approved First, Not Last

Think of pre-approval like setting your GPS before a road trip.

We help you understand:

What monthly payment is realistic for your lifestyle

How to structure the loan so you don’t overpay on interest

What price range keeps your total cost of homeownership affordable

Bonus: You’ll be taken more seriously by sellers and agents once you're pre-approved.

3. Expand the Location Map

Clarkston is wonderful—but it’s not the only place you can find value.

Consider nearby communities like:

Davisburg

Holly

Ortonville

Lapeer

Many of these areas qualify for USDA no-down-payment loans and have lower average home prices than closer-in suburbs.

4. Think Like a House Hacker

You’ve heard of roommates—what about tenants?

Some Millennial buyers are purchasing homes with:

Basements they can rent out

Garage apartments or ADUs

Multifamily homes (duplex, triplex, etc.)

This rental income can offset your mortgage—and in many cases, help you qualify for more.

5. Refinance Later—Buy the Right Home Now

Here’s a truth bomb: You marry the house, not the rate.

Yes, rates are higher than they were in 2021. But once you're in the home, you can always:

Refinance when rates drop (we monitor this for you)

Tap into equity later for renovations or debt consolidation

Start building wealth now—because rent doesn’t give you equity

Waiting might cost you more if prices keep climbing.

🤔 Is Now Really a Good Time to Buy?

For many Millennials, yes—but only if the numbers work for your situation.

Here’s how I help my clients decide:

✅ Run a Total Cost Analysis showing rent vs. buy over 5–10 years

✅ Explore multiple loan options to fit your goals

✅ Plan for future refinancing and equity growth

✅ Connect you with trusted local realtors and financial planners

📍 Let’s Talk About Your Plan (No Pressure)

Whether you’re ready to go or just starting to explore, I’m here to help.

You deserve to own a home that fits your budget and your lifestyle.

Let’s figure out a strategy that works for you—no pushy sales talk, just real guidance.

📞 Erik Gascho

Clarkston Mortgage Expert – NEO Home Loans powered by Better

📍 Serving Clarkston, Waterford, Holly, and all of Southeast Michigan

📅 Schedule a Free Planning Call

📱 248-214-8526

For decades, most mortgage lending has relied on Classic FICO.

Classic FICO gives lenders a snapshot of your credit at one point in time. It looks at things like payment history, balances, length of credit, credit mix, and recent credit activity.

Many homeowners feel stuck.

On one hand, you may have a mortgage rate that’s far lower than today’s market rates. Giving that up can feel like a mistake.

Homeownership is not just about getting the keys.

It is about caring for the place you live, protecting the investment you made, and making smart financial decisions along the way. At NEO Home Loans, we believe successful homeownership is built one month at a time through education, planning, and proactive support.

Do we make an offer and hope everything works out?

Do we wait and risk losing the home?

Do we rush our current home onto the market?

Unfortunately, this is where many homeowners find themselves.

Nobody wants to feel like they bought at the “wrong time.” Especially after watching headlines bounce between “housing crash,” “record prices,” and “rates are too high.”

If you’re thinking about moving, you’ve probably run into this problem:

You want to buy your next home…

But you feel like you have to sell your current one first.

When most people look at a mortgage payment, they only see what it costs today.

But that may not be the best question.

A better question could be:

What will this same payment feel like 10 years from now?

The housing market is changing… and most buyers haven’t caught up yet.

For the past few years, sellers had all the control. Homes sold fast. Buyers competed aggressively. And negotiating power was almost nonexistent.

That’s no longer the case.

Today, we’re seeing a clear shift toward a more balanced market, and that creates opportunity if you know how to use it.

If you’re planning to buy a home this season, you’re stepping into a market full of opportunity.

More homes are coming to market. Activity is picking up. And it finally feels like you might have a real shot at finding the right home.

But there’s a challenge most buyers don’t realize until it’s too late.

Discover why focusing only on interest rates can cost Michigan homeowners thousands. Learn how mortgage strategy impacts long-term wealth.