Mortgage Rates & Market Uncertainty: What Clarkston Homebuyers Need to Know Right Now

Erik Gascho • July 28, 2025

Tariffs, the Fed, and Your Mortgage: What’s Driving Rates in Clarkston This Week?

🌪️ Market Whirlwind: What’s Going On?

It’s been a bumpy few weeks in the financial markets—and if you’re a homebuyer, homeowner, or real estate agent in Clarkston, Waterford, or the greater Oakland County area, you’ve likely noticed mortgage rates jumping around again. Let’s break down why this is happening and what it means for your next move.

1. 📦 Tariffs + Trade Tensions = Higher Inflation Risk

Late last week, headlines buzzed with news of proposed tariffs on Chinese electric vehicles and technology components. While this may seem distant from your local real estate market, these policies have a ripple effect. Why?

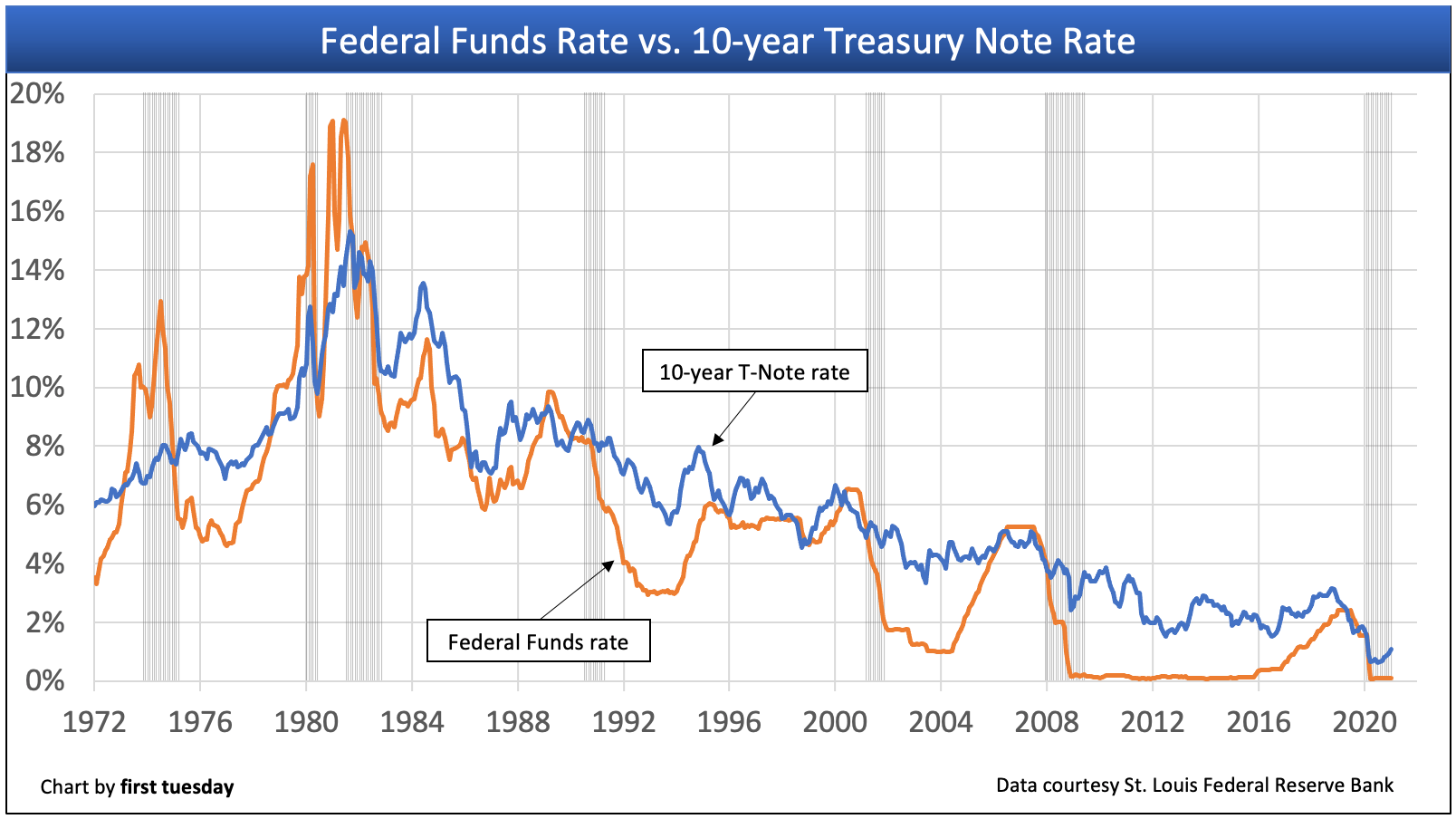

Tariffs often lead to higher consumer prices, which fuels inflation. And when inflation rises, mortgage rates usually follow suit—because lenders demand higher returns to keep up with the cost of living.

2. 🏦 The Fed Is Watching… and Waiting

The Federal Reserve met again this month, and while they chose to hold rates steady, their tone was anything but dovish. Chair Jerome Powell emphasized that "more confidence" is needed before rate cuts can begin.

Translation: The Fed wants to see clear, sustained progress on inflation before acting—and recent economic data has been mixed.

Here’s the tricky part: while the Fed doesn’t set mortgage rates directly, its actions heavily influence investor behavior in the bond market, which directly drives mortgage rates.

👀 Local Note: In Michigan, inflation has remained slightly below the national average, but rising auto insurance and utility costs are pushing household budgets tighter—something the Fed is monitoring closely.

3. 💵 Mortgage Rates: What We’re Seeing Now

As of today, average 30-year fixed mortgage rates are hovering in the high 6% to low 7% range, depending on credit score and loan type. Rates dipped slightly last week, but volatility is high due to the tug-of-war between inflation concerns and cooling economic data.

If you’re waiting for “the perfect time” to buy or refinance, this market may feel like a moving target.

🔍 What Should You Do Right Now?

Let’s make this simple.

👉 If You’re a Homebuyer in Clarkston or Nearby:

Don’t wait for rates to drop dramatically. We’re unlikely to see a sharp decline unless economic conditions worsen significantly.

Get fully pre-approved today. Locking in a rate protects you from future spikes while shopping.

Explore rate buydown strategies or builder-paid closing costs in areas like Grand Blanc and White Lake, where incentives are common.

👉 If You’re a Homeowner:

Monitor your current rate. If you’re in the 7s or higher, a refinance might make sense if we dip back into the 6s.

Consider a home equity strategy. Rising home values in Clarkston mean more tappable equity—potentially useful for debt consolidation or renovation.

💬 Let’s Talk: No Pressure, Just a Plan

I get it—this market feels uncertain. But here’s the truth: uncertainty creates opportunity for those who are informed and proactive.

If you’d like a custom mortgage review, a second opinion, or just someone to explain what’s really going on without all the noise, let’s connect.

📅 Book a free call here: erikgascho.youcanbook.me

📱 Or text me directly at 248-214-8526

For decades, most mortgage lending has relied on Classic FICO.

Classic FICO gives lenders a snapshot of your credit at one point in time. It looks at things like payment history, balances, length of credit, credit mix, and recent credit activity.

Many homeowners feel stuck.

On one hand, you may have a mortgage rate that’s far lower than today’s market rates. Giving that up can feel like a mistake.

Homeownership is not just about getting the keys.

It is about caring for the place you live, protecting the investment you made, and making smart financial decisions along the way. At NEO Home Loans, we believe successful homeownership is built one month at a time through education, planning, and proactive support.

Do we make an offer and hope everything works out?

Do we wait and risk losing the home?

Do we rush our current home onto the market?

Unfortunately, this is where many homeowners find themselves.

Nobody wants to feel like they bought at the “wrong time.” Especially after watching headlines bounce between “housing crash,” “record prices,” and “rates are too high.”

If you’re thinking about moving, you’ve probably run into this problem:

You want to buy your next home…

But you feel like you have to sell your current one first.

When most people look at a mortgage payment, they only see what it costs today.

But that may not be the best question.

A better question could be:

What will this same payment feel like 10 years from now?

The housing market is changing… and most buyers haven’t caught up yet.

For the past few years, sellers had all the control. Homes sold fast. Buyers competed aggressively. And negotiating power was almost nonexistent.

That’s no longer the case.

Today, we’re seeing a clear shift toward a more balanced market, and that creates opportunity if you know how to use it.

If you’re planning to buy a home this season, you’re stepping into a market full of opportunity.

More homes are coming to market. Activity is picking up. And it finally feels like you might have a real shot at finding the right home.

But there’s a challenge most buyers don’t realize until it’s too late.

Discover why focusing only on interest rates can cost Michigan homeowners thousands. Learn how mortgage strategy impacts long-term wealth.