Why My Mortgage Under Management™ System Means You'll Never Overpay Again

Erik Gascho • July 29, 2025

Your Mortgage Shouldn’t Be “Set It and Forget It”

Most people think of their mortgage as a one-time decision—get the loan, make your payments, and forget about it. But in today’s rapidly changing market, that approach can cost you thousands over time.

That’s why I take a different approach.

As a Mortgage Advisor based in Clarkston, Michigan, I offer all of my clients a proactive strategy called Mortgage Under Management™—a system designed to make sure you never overpay on your mortgage.

What Is Mortgage Under Management?

Just like a financial advisor manages your investments, I manage your mortgage. My Mortgage Under Management™ (MUM) system is a full-lifecycle strategy that monitors:

Interest rate trends

Loan program changes

Your home equity growth

Your financial goals

Potential refinance opportunities

Think of it as a personal mortgage watchtower—constantly scanning the horizon for ways to save you money or create financial flexibility.

How I Make Sure You Never Overpay

Here’s exactly how the system works:

1. Initial Planning That Aligns With Your Goals

Whether you're buying in Clarkston, Lake Orion, Rochester, or anywhere in Metro Detroit, we start by understanding your bigger picture:

Are you planning to move in 5 years?

Is college planning a factor?

Do you expect your income or family situation to change?

We build your mortgage around life planning, not just interest rates.

2. Ongoing Rate Monitoring

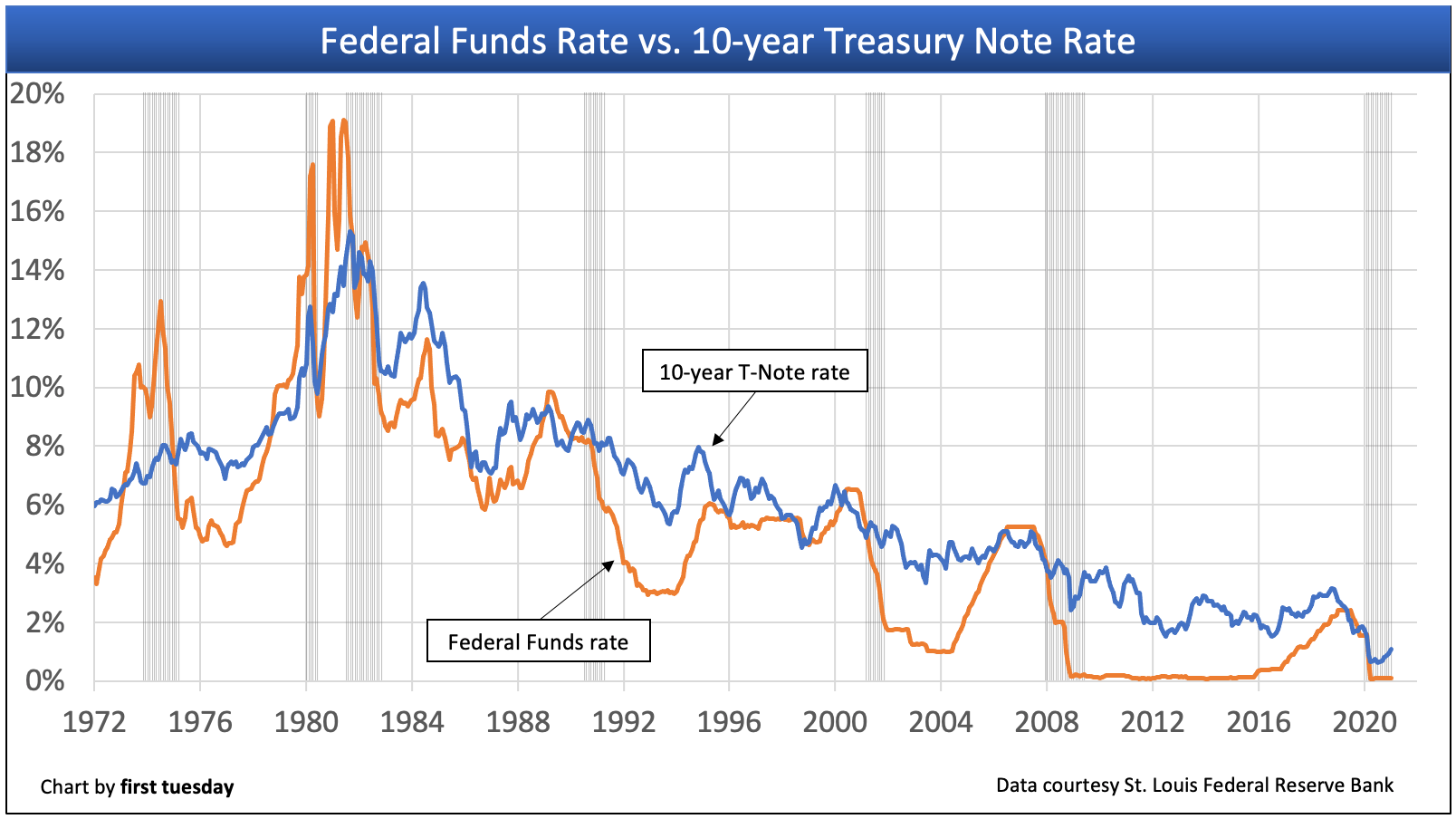

Once you're in your mortgage, I don’t walk away. I track the market daily for rate movements that might create a refinancing opportunity.

If a better rate becomes available that aligns with your financial goals, I’ll let you know—without you needing to ask.

💡 Example: One Clarkston client refinanced 18 months after closing, saving $294/month because our monitoring system caught a drop during a short-term rate dip.

3. Monthly Equity Reviews

As home values continue to shift in Oakland County, it’s important to keep tabs on your equity. We send out quarterly equity updates that show:

Your estimated home value

Remaining loan balance

Opportunities for debt consolidation or cash-out

4. Refi Triggers + Alerts

Using technology (and some smart math), I set a personalized Rate Watch system for every client. If your loan hits a savings threshold (for example, $150+ per month net savings), we trigger a custom review.

This means you're not reacting to market hype—you’re responding to real, personalized savings opportunities.

Why This Matters More Than Ever in 2025

As of this summer, Michigan mortgage rates are hovering around 6.75–7.25% depending on credit, down payment, and program. But volatility is high, and the window for optimal refinancing can be short.

Timing the market on your own is risky and stressful.

But with Mortgage Under Management™, you don’t have to guess. I watch the market so you don’t have to—and I’ll guide you when it’s time to act.

Who This Helps Most

✅ First-time buyers in Clarkston who want long-term guidance

✅ Homeowners who bought in 2022–2024 when rates were elevated

✅ Families looking to consolidate debt or free up monthly cash flow

✅ Professionals planning for financial growth or early retirement

How to Get Started

If you want someone in your corner watching the market for you, let’s connect.

📅 Book a Free Mortgage Review

📞 Or call/text me at 248-214-8526

📍 Based in Clarkston, Michigan, proudly serving Lake Orion, Oxford, Rochester, and all of Oakland County.

Final Thought

A mortgage shouldn’t be a set-it-and-forget-it loan. With my Mortgage Under Management™ system, you can rest easy knowing you’ll never overpay—because I’m always looking out for the next opportunity to improve your financial position.

You focus on living your life. I’ll handle the mortgage.

For decades, most mortgage lending has relied on Classic FICO.

Classic FICO gives lenders a snapshot of your credit at one point in time. It looks at things like payment history, balances, length of credit, credit mix, and recent credit activity.

Many homeowners feel stuck.

On one hand, you may have a mortgage rate that’s far lower than today’s market rates. Giving that up can feel like a mistake.

Homeownership is not just about getting the keys.

It is about caring for the place you live, protecting the investment you made, and making smart financial decisions along the way. At NEO Home Loans, we believe successful homeownership is built one month at a time through education, planning, and proactive support.

Do we make an offer and hope everything works out?

Do we wait and risk losing the home?

Do we rush our current home onto the market?

Unfortunately, this is where many homeowners find themselves.

Nobody wants to feel like they bought at the “wrong time.” Especially after watching headlines bounce between “housing crash,” “record prices,” and “rates are too high.”

If you’re thinking about moving, you’ve probably run into this problem:

You want to buy your next home…

But you feel like you have to sell your current one first.

When most people look at a mortgage payment, they only see what it costs today.

But that may not be the best question.

A better question could be:

What will this same payment feel like 10 years from now?

The housing market is changing… and most buyers haven’t caught up yet.

For the past few years, sellers had all the control. Homes sold fast. Buyers competed aggressively. And negotiating power was almost nonexistent.

That’s no longer the case.

Today, we’re seeing a clear shift toward a more balanced market, and that creates opportunity if you know how to use it.

If you’re planning to buy a home this season, you’re stepping into a market full of opportunity.

More homes are coming to market. Activity is picking up. And it finally feels like you might have a real shot at finding the right home.

But there’s a challenge most buyers don’t realize until it’s too late.

Discover why focusing only on interest rates can cost Michigan homeowners thousands. Learn how mortgage strategy impacts long-term wealth.